Analysis of the status quo of China's titanium alloy industry in 2020, the high-end market is highly concentrated and the market is developing steadily

1. Overview of the titanium alloy industry

Although titanium alloy has good properties, it is very difficult to process. When the Brinell hardness is less than 300, the sticking is serious; when it is greater than 370, it is too hard to process, and most of the titanium alloys have low thermal conductivity. The heat generated during the processing will not be quickly transferred to the workpiece, but will be concentrated The cutting area, on the one hand, will quickly wear the tool, and on the other hand, it will destroy the surface integrity of the part, resulting in a decrease in the geometric accuracy of the part and the phenomenon of work hardening. In particular, military titanium materials of certain types generally require multiple plastic processing. How to ensure uniform and stable quality and achieve industrialized mass production is a technical challenge in the world. At present, only the United States, Russia, Japan, China, and the former CIS (Ukraine and Kazakhstan) five countries and regions have a complete titanium processing and manufacturing process.

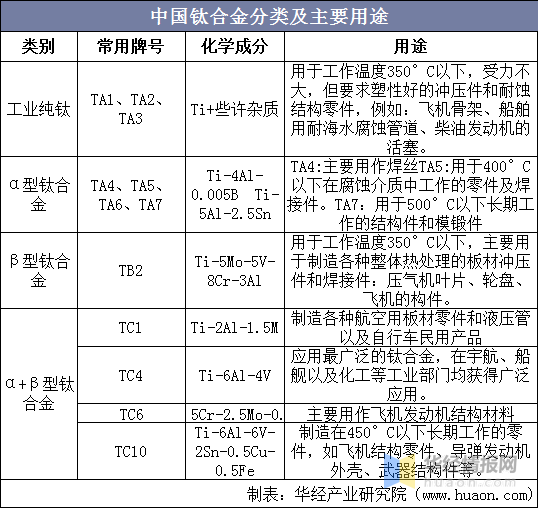

In terms of classification, titanium alloys can be divided into industrial pure titanium, α-type titanium alloy, β-type titanium alloy and α+β-type titanium alloy. Different structures are made according to different purposes, and they are widely used in aviation, chemical and metallurgical industries. .

Data source: public data collation

2. Overall analysis of the titanium alloy industry chain

(1) The overall industry chain

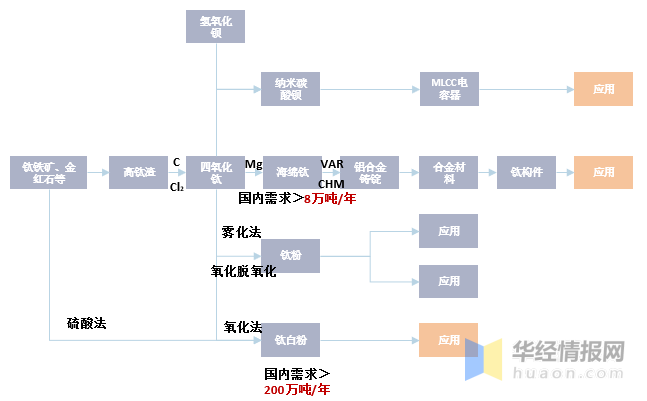

The titanium alloy industry chain generally covers three parts: the preparation of sponge titanium, the preparation of titanium materials and the application of titanium materials. The first two parts are complicated in technology and difficult to prepare. They are the difficulties and key links in the application of titanium. The quality of titanium sponge and titanium materials directly determines titanium. Product quality. The titanium industry is a technology and capital-intensive industry with complex smelting technology, high processing difficulty, and high technical content. At present, the main bottleneck lies in high production costs and expensive titanium materials, which restricts its output increase and promotion and application. In the future, with the improvement of titanium smelting and processing technology, the cost will inevitably be reduced. The characteristics of titanium must make it have a significant substitution effect relative to other metals. The future development of the titanium industry is quite broad.

Schematic diagram of the titanium alloy industry chain

Data source: public data collation

(2) Upstream raw materials

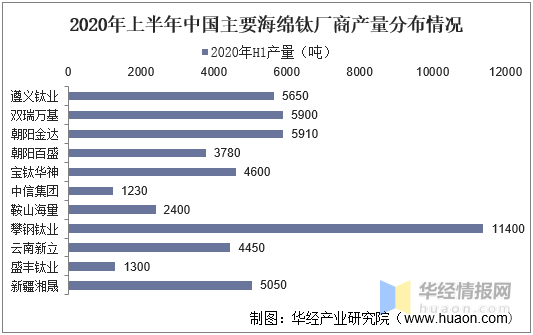

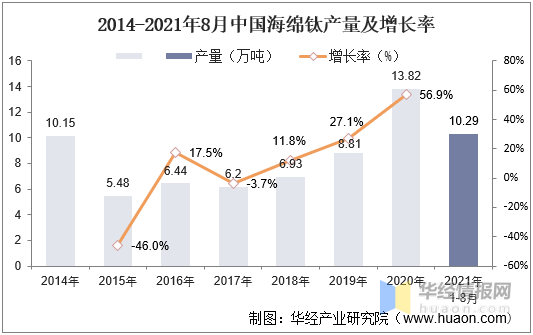

Titanium sponge is the main upstream raw material of titanium alloys. After the changes in the period from 2014 to 2015, the output of titanium sponge in my country has dropped sharply. The output in 2015 was 54785 tons, a year-on-year decrease of 46.02%. With the broadening of high-end titanium alloy applications, 2015 -In 2019, my country's titanium sponge production continued to grow, from 54,800 tons to 88,100 tons, with a compound annual growth rate of 12.61%. The industry continued to recover in 2020, and the production of sponge titanium reached 138,200 tons, an increase of 56.9% year-on-year. The output from January to August in 2021 is 102,900 tons.

Source: China Nonferrous Metals Industry Association, Huajing Industry Research Institute

As the world's largest producer of titanium sponge, China has been gradually eliminating and shutting down most of its backward production capacity under the policy guidelines of "three removals, one reduction and one supplement" in supply-side reforms and the high pressure of the "environmental storm" in recent years, and industrial concentration continues With the increase, the capacity utilization rate once rebounded to nearly 80%, and the demand structure has shifted from the past low-end to high-end fields such as military equipment. In 2019, driven by the gradual construction of private petroleum refining and chemical projects and the accelerated installation of national defense and military equipment, the demand for military and civilian titanium sponge has increased significantly, attracting a large number of domestic manufacturers such as Xinjiang Xiangsheng and Yunnan Xinli to resume production and expand capacity. Production capacity increased significantly by 42% to 157,000 tons. However, due to the fact that downstream demand growth is not as fast as production capacity, the annual output in 2019 was only 85,000 tons, and the capacity utilization rate dropped to 54%, a record low in the past five years.

Data source: public data collation

(3) Downstream structure

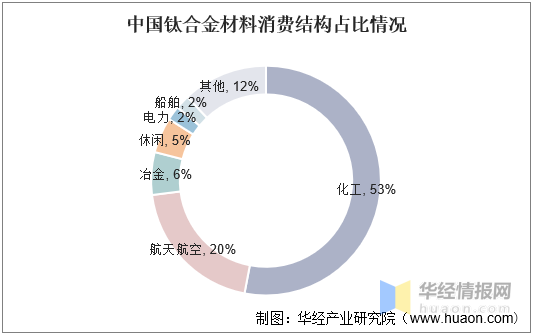

In the domestic titanium alloy consumption structure, the chemical industry accounts for a large proportion, accounting for about 53%, and aerospace accounts for the second, about 21%, which is much lower than the international average of about 50%. There is still great potential in the aviation titanium material market.

Data source: public data collation

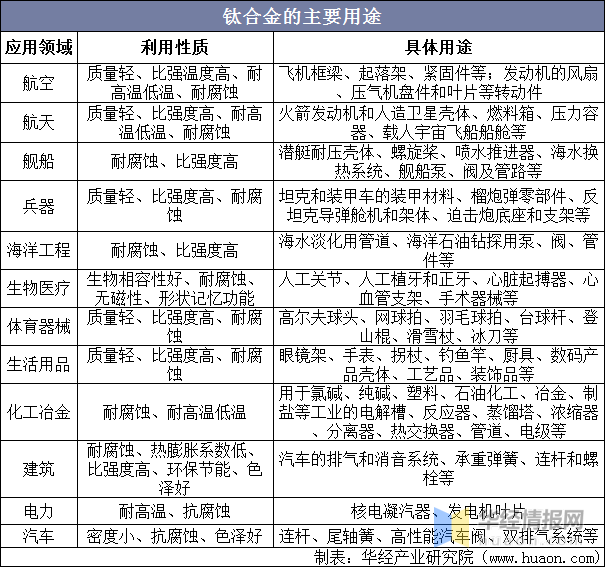

The density of titanium alloy is generally 4.5g/cm3, which is only 60% of steel. The strength of pure titanium is close to that of ordinary steel. Therefore, some high-strength titanium alloys exceed the strength of many alloys. Titanium alloy has the characteristics of high unit strength, good rigidity, high thermal strength, corrosion resistance, good high and low temperature resistance, and low thermal conductivity. It can be used as corrosion-resistant lightweight structural materials, new functional materials and important bioengineering materials. At present, titanium alloys have been widely used in military and civilian fields such as aerospace, weapons, chemistry, metallurgy, naval industry, and marine development.

Data source: public data collation

3. The status quo of the titanium alloy market

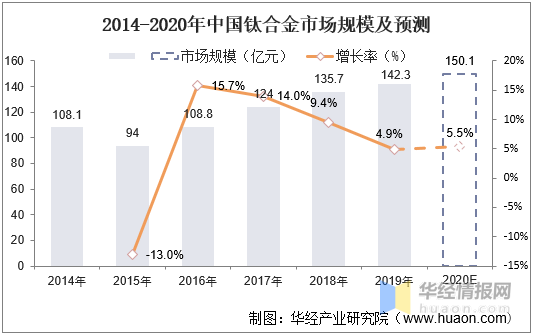

(1) Market size

From 2014 to 2015, affected by the adjustment of my country's national economic structure, the output of titanium sponge in the upstream declined rapidly and the demand for titanium alloys in traditional industrial fields such as downstream traditional chemical industry and metallurgy declined, resulting in a decline in the output value of titanium alloys and accompanying the adjustment of my country's industrial structure. Initial results have been achieved. High-end titanium alloy applications such as aerospace and marine engineering have achieved rapid development. After 2015, the output value of titanium alloys has increased steadily. From 2014 to 2019, the market size of my country's titanium alloy industry increased from 10.81 billion yuan to 14.23 billion yuan, with a compound annual growth rate of 7.11%. In the context of the continuous adjustment and upgrading of my country's industrial structure, the market for high-end titanium alloys is huge, and the demand for high-end titanium alloys with high added value will steadily increase. It is expected that the market size of my country's titanium alloy industry will exceed 15 billion yuan in 2020.

Data source: public data collation

Related report: "China's Titanium Alloy Market Competitive Strategy and Industry Investment Potential Forecast Report 2021-2026" issued by Huajing Industry Research Institute.

(2) Competitive landscape

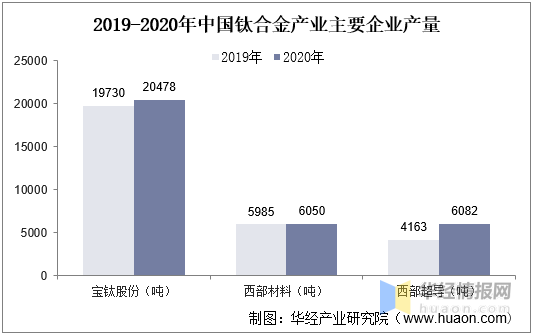

At present, the main companies in my country's titanium alloy industry are Western Superconductor (mainly rods and wires), Western Materials, and Baoti Co., Ltd. (complete quality, self-sufficient titanium sponge and export). Orders for high-end titanium materials are concentrated in the two leaders of Western Superconductor and Baoti Co., Ltd., which together account for more than 95% of the market share, and have formed a relatively stable duopoly competition pattern. Western Superconductor mainly focuses on rods and wires, focusing on the aviation field. Baoti has a complete range of products. Plates, ribbons, tubes, rods, wires, etc. are widely used in aerospace and are also worthy of attention.

Data source: public data collation

4. The development trend of titanium alloy industry

(1) Recent price increases

Driven by demand, the overall price of titanium alloys has increased significantly. Take the titanium plate with a relatively simple processing level as an example. In October 20, the price of titanium plate was 94 yuan/kg, and the ex-factory price reached 127 yuan/kg in October 21, an increase of 35%. The price of titanium alloy varies with the level of processed materials and product forms. The higher the processing level, the higher the corresponding price and the higher the profit margin.

(2) Policies help industry development

The titanium industry has an important position in the development of the national economy and is of strategic significance to the development of national defense, economy and technology. It is an important raw material industry that supports the advancement of cutting-edge science and technology, and is also a basic industry for the development of the national economy and industrial upgrading. my country attaches great importance to the development of the titanium industry. The titanium industry is supported by the state and local governments at all levels, and Shaanxi Province has listed it as an economic pillar industry.

TEL

TEL